The Ultimate Guide to Securing a Mortgage with Low Credit Scores: Securing a mortgage can feel daunting, especially with a less-than-perfect credit score. This guide demystifies the process, offering practical strategies and valuable insights to help you navigate the complexities of mortgage lending and achieve your homeownership dreams, even with a lower credit rating. We’ll explore various mortgage options, effective credit improvement techniques, and crucial steps to increase your chances of approval.

From understanding the factors that influence your credit score to negotiating favorable loan terms and avoiding predatory lending practices, this comprehensive guide provides a roadmap to success. We’ll cover everything from improving your credit score to finding the right lender and preparing your financial documents. Learn how to effectively communicate with lenders, understand mortgage insurance, and maintain a healthy financial situation after securing your mortgage. This guide empowers you to take control of your financial future and achieve your homeownership goals.

Understanding Credit Scores and Mortgage Eligibility

Securing a mortgage can be a significant financial undertaking, and your credit score plays a crucial role in determining your eligibility and the terms you’ll receive. Understanding how credit scores are calculated and their impact on mortgage approvals is essential for navigating the process successfully. This section will detail the factors influencing credit scores, their effect on mortgage approval, and illustrate how specific credit score elements affect interest rates.

Factors Influencing Credit Scores

Credit scores are numerical representations of your creditworthiness, calculated using a complex algorithm that considers several key factors. These factors are weighted differently by various credit scoring models (like FICO and VantageScore), but generally include payment history, amounts owed, length of credit history, credit mix, and new credit.

Payment history is the most significant factor, accounting for approximately 35% of your FICO score. Consistent on-time payments demonstrate responsible financial behavior, while late or missed payments negatively impact your score. Amounts owed, representing your credit utilization ratio (the percentage of available credit you’re using), accounts for about 30%. Keeping your credit utilization low (ideally below 30%) is crucial. Length of credit history (15%) reflects the age of your oldest account and the average age of all your accounts. A longer credit history generally suggests greater financial responsibility. Credit mix (10%) refers to the variety of credit accounts you possess (credit cards, loans, etc.). A diverse mix can positively influence your score. Finally, new credit (10%) considers the number of recent credit applications. Multiple applications in a short period can temporarily lower your score.

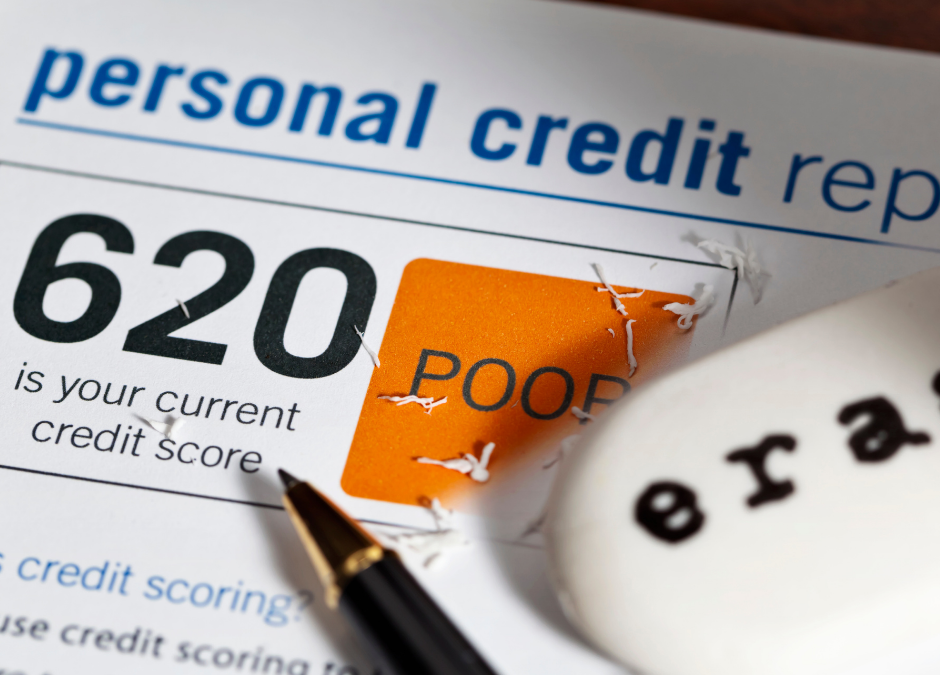

Impact of Credit Score Ranges on Mortgage Approval

Your credit score directly impacts your mortgage eligibility and the terms you’ll receive. Lenders use credit scores to assess risk; a higher score indicates a lower risk of default, making you a more attractive borrower. Generally, borrowers with scores above 660 are considered to have good credit, while scores below 620 are often viewed as having poor credit.

Borrowers with excellent credit scores (750 and above) typically qualify for the best mortgage rates and terms, including lower interest rates, potentially larger loan amounts, and a wider variety of loan options. Those with good credit (660-749) usually qualify for mortgages but may face slightly higher interest rates. Individuals with fair credit (620-659) may still qualify, but securing a mortgage might be more challenging, requiring a larger down payment or higher interest rates. Borrowers with poor credit (below 620) often face significant challenges obtaining a mortgage, potentially requiring significant improvements to their credit scores before approval. In some cases, they may only qualify for higher-interest rate loans or specialized programs designed for borrowers with impaired credit.

Examples of How Credit Score Factors Affect Interest Rates

Let’s illustrate the impact of credit scores on interest rates with a few examples. Assume a $300,000 mortgage over 30 years. A borrower with an excellent credit score (780) might qualify for a 4% interest rate, resulting in significantly lower monthly payments and total interest paid over the life of the loan compared to a borrower with a fair credit score (630) who might receive a 6% interest rate. The difference in interest rates can translate into thousands of dollars in additional costs over the loan term. Even a small difference in credit score can significantly impact the interest rate offered. For example, a borrower with a score of 720 might receive a 4.5% rate, while a borrower with a 700 score might receive a 5% rate.

Credit Score Ranges and Associated Mortgage Options

The following table summarizes the general relationship between credit score ranges and associated mortgage options. Keep in mind that these are general guidelines, and individual lender policies and market conditions can influence the actual terms offered.

| Credit Score Range | Mortgage Options | Interest Rate Expectation | Down Payment Requirement |

|---|---|---|---|

| 750+ (Excellent) | Wide range of options, including conventional, FHA, VA | Lowest available rates | Potentially lower down payment options |

| 660-749 (Good) | Most conventional loan options available | Competitive rates | Standard down payment requirements |

| 620-659 (Fair) | Limited options; may require higher down payments or private mortgage insurance (PMI) | Higher interest rates | Higher down payment requirements |

| Below 620 (Poor) | Securing a mortgage may be difficult; specialized programs or significantly higher interest rates | Substantially higher interest rates | Very high down payment requirements or potentially impossible |

Improving Your Credit Score Before Applying

Securing a mortgage with a low credit score can be challenging, but significantly improving your score before applying is achievable with focused effort and strategic planning. By implementing the strategies outlined below, you can demonstrably increase your chances of mortgage approval and potentially qualify for better interest rates. Remember, consistent effort is key to seeing positive results.

Improving your credit score involves a multifaceted approach focusing on responsible financial behavior and proactive credit management. The most effective strategies center around consistently paying bills on time, actively managing debt, and ensuring the accuracy of your credit report. These actions, when performed consistently, will lead to a noticeable improvement in your credit score over time.

Paying Bills on Time and Managing Debt

Prompt and consistent bill payments are paramount to improving your credit score. Payment history constitutes a significant portion (35%) of your FICO score, the most widely used credit scoring model. Even a single late payment can negatively impact your score, while a history of on-time payments significantly boosts it. Effective debt management is equally crucial. High credit utilization (the amount of credit you’re using compared to your total available credit) can negatively affect your score. Aim to keep your credit utilization below 30%, ideally closer to 10%. Strategies like creating a budget, prioritizing high-interest debt, and exploring debt consolidation options can help manage debt effectively. For example, consistently paying off your credit card balances in full each month will significantly improve your credit utilization ratio.

Disputing Inaccurate Credit Report Information

Errors on your credit report can significantly lower your credit score. Regularly reviewing your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion) is essential. If you discover any inaccuracies, such as incorrect account information, late payments that weren’t actually late, or accounts that don’t belong to you, dispute them immediately with the respective credit bureau. Provide supporting documentation, such as payment receipts or account statements, to strengthen your case. Successfully resolving inaccuracies can lead to a substantial increase in your credit score. For instance, removing a wrongly reported collection account could significantly improve your score.

A Step-by-Step Guide for Improving Credit Scores Within Six Months

Improving your credit score within six months requires dedication and consistent effort. Follow these steps:

- Obtain your credit reports: Request your free credit reports from AnnualCreditReport.com to identify areas for improvement.

- Pay all bills on time: Set up automatic payments or reminders to ensure timely payments. Even a single missed payment can have a negative impact.

- Reduce credit utilization: Aim to keep your credit utilization below 30% by paying down existing balances and avoiding opening new credit accounts unnecessarily.

- Dispute any errors: Carefully review your credit reports for inaccuracies and submit disputes with the appropriate credit bureaus.

- Maintain a mix of credit accounts: A diverse credit history, including installment loans (like auto loans or personal loans) and revolving credit (like credit cards), can positively influence your score. However, avoid opening new accounts solely for this purpose.

- Monitor your progress: Track your credit score regularly to gauge the effectiveness of your efforts. Consider using a credit monitoring service.

Remember, improving your credit score takes time and consistent effort. While significant improvements within six months are possible, the exact timeframe depends on individual circumstances and the severity of credit issues. Consistent application of these strategies will increase your likelihood of success.

Exploring Mortgage Options for Low Credit Scores

Securing a mortgage with a low credit score can feel daunting, but it’s not impossible. Several mortgage options cater specifically to borrowers with less-than-perfect credit. Understanding the nuances of these programs is crucial to finding the best fit for your financial situation. This section will explore some of the most common options, comparing their interest rates, terms, and eligibility requirements.

FHA Loans

FHA loans, insured by the Federal Housing Administration, are designed to help individuals with lower credit scores become homeowners. They require a lower down payment than conventional loans and generally have more lenient credit score requirements.

- Interest Rates and Terms: FHA loan interest rates are typically higher than those for conventional loans with higher credit scores, reflecting the higher risk for lenders. Terms can vary, but 15- and 30-year mortgages are common.

- Requirements and Eligibility Criteria: While specific requirements can vary by lender, generally, you’ll need a credit score above 500 (with a 10% down payment) or 580 (with a 3.5% down payment). You’ll also need to meet income requirements and demonstrate the ability to repay the loan.

- Pros: Lower down payment requirements, more lenient credit score requirements, easier qualification process than conventional loans.

- Cons: Higher interest rates compared to conventional loans, mortgage insurance premiums (MIP) are required for the life of the loan or until a certain percentage of equity is built.

VA Loans

VA loans, guaranteed by the Department of Veterans Affairs, are available to eligible veterans, active-duty military personnel, and surviving spouses. They offer several advantages, including no down payment requirement and competitive interest rates.

- Interest Rates and Terms: VA loan interest rates are generally competitive, often comparable to or slightly higher than conventional loans, depending on market conditions and the borrower’s credit score. Loan terms are typically 15 or 30 years.

- Requirements and Eligibility Criteria: Eligibility depends on military service history. Credit score requirements are generally less stringent than conventional loans, though lenders may still consider your creditworthiness. A Certificate of Eligibility (COE) is required to apply.

- Pros: No down payment required, competitive interest rates, no private mortgage insurance (PMI) required.

- Cons: Eligibility is restricted to qualified veterans and their families, funding fee is usually required (though it can be financed into the loan), appraisal and closing costs still apply.

USDA Loans

USDA loans, backed by the U.S. Department of Agriculture, are designed to assist low-to-moderate-income homebuyers in rural areas. These loans often offer attractive terms, including low or no down payment options.

- Interest Rates and Terms: Interest rates on USDA loans are typically competitive, though they can vary depending on the market and the borrower’s credit score. Loan terms are usually 30 years.

- Requirements and Eligibility Criteria: Borrowers must meet income limits and purchase a home in a designated rural area. Credit score requirements are generally less stringent than conventional loans, but lenders will assess creditworthiness.

- Pros: Low or no down payment required, competitive interest rates, available in rural areas.

- Cons: Limited to rural areas, income restrictions apply, guarantee fee is required.

Finding a Lender Who Specializes in Low Credit Score Mortgages

Securing a mortgage with a less-than-perfect credit score can feel daunting, but it’s achievable with the right approach. Finding a lender who understands your situation and offers suitable mortgage options is crucial. This section will guide you through the process of identifying and evaluating lenders specializing in mortgages for borrowers with low credit scores.

Finding the right lender requires proactive research and careful comparison. Not all lenders are created equal, and some are more willing to work with borrowers who have experienced credit challenges than others. Understanding their lending criteria and fees is essential to making an informed decision.

Identifying Lenders Specializing in Low Credit Score Mortgages

Several avenues exist for finding lenders who cater to borrowers with lower credit scores. These include online search engines, referrals from financial advisors, and direct outreach to lenders known for their flexible lending practices. It’s important to carefully examine each lender’s stated criteria and past performance before submitting an application. Focusing your search on lenders advertising programs specifically designed for those with less-than-perfect credit significantly increases your chances of approval.

Utilizing Resources for Researching Reputable Lenders

Reliable resources exist to assist in your search for reputable lenders. Consumer financial protection agencies often publish lists of licensed and compliant lenders, allowing you to cross-reference your potential lenders against these lists. Independent financial websites also provide ratings and reviews of mortgage lenders, offering valuable insights into their customer service, approval rates, and overall reputation. Using these resources reduces the risk of encountering predatory lenders who may exploit borrowers in vulnerable financial situations.

Comparing Lender Offers and Fees

Once you’ve identified several potential lenders, carefully compare their offers and associated fees. This includes not only the interest rate but also closing costs, points, and any other charges. A seemingly lower interest rate may be offset by significantly higher fees, ultimately resulting in a more expensive mortgage. Creating a detailed comparison table allows for easy side-by-side evaluation of different lender offerings. This meticulous comparison helps you identify the most cost-effective option.

Checklist for Evaluating Potential Lenders

Before committing to a lender, use this checklist to ensure a thorough evaluation:

| Criterion | Evaluation |

|---|---|

| Interest Rate | Record the annual percentage rate (APR) offered. |

| Loan Fees | List all fees, including origination fees, appraisal fees, and closing costs. |

| Loan Terms | Note the loan term (e.g., 15 years, 30 years) and any prepayment penalties. |

| Credit Score Requirements | Clarify the minimum credit score required for approval. |

| Customer Reviews | Review online ratings and customer testimonials to gauge the lender’s reputation. |

| Licensing and Accreditation | Verify the lender’s licensing and accreditation with relevant authorities. |

| Transparency of Fees | Ensure all fees are clearly explained and itemized. |

Preparing Your Financial Documents

Securing a mortgage, even with a low credit score, requires meticulous preparation of your financial documents. Lenders need a comprehensive picture of your financial health to assess your ability to repay the loan. Providing accurate and complete documentation demonstrates your commitment and increases your chances of approval. Incomplete or inaccurate information can significantly delay the process or even lead to rejection.

Providing accurate and complete financial documentation is crucial for a successful mortgage application. Lenders use this information to verify your income, assets, debts, and overall financial stability. Errors or omissions can raise red flags and lead to delays or denial of your application. Thorough preparation minimizes these risks and demonstrates your seriousness as a borrower.

Necessary Documents for Mortgage Application

The specific documents required may vary slightly depending on the lender and your individual circumstances. However, the following list represents a common set of documents you should anticipate needing. Gathering these documents in advance will streamline the application process.

- Proof of Income: This typically includes your most recent two years’ W-2 forms, pay stubs from the last 30-60 days, tax returns (including all schedules), and possibly bank statements showing direct deposit of income.

- Bank Statements: Provide bank statements for the past two to three months from all your accounts (checking, savings, money market). These demonstrate your cash flow and savings habits.

- Asset Documentation: Documentation proving ownership and value of any assets you intend to use for the down payment or closing costs. This may include statements for investment accounts, retirement accounts (401k, IRA), and stock portfolios.

- Debt Documentation: A list of all your outstanding debts, including credit card balances, auto loans, student loans, and other installment loans. You will likely need to provide statements or account information for each.

- Government-Issued Identification: A valid driver’s license or passport is essential for verification of identity.

- Proof of Residence: Utility bills, rental agreements, or other documentation proving your current address.

- Employment Verification: In some cases, lenders may request direct verification of your employment from your employer.

Organizing and Presenting Financial Information

Effective organization of your financial documents is essential for a smooth application process. A well-organized application demonstrates professionalism and saves time for both you and the lender.

- Create a Dedicated File: Designate a physical or digital folder to store all mortgage-related documents. Maintain a clear and organized system for easy access.

- Accurate and Complete Information: Ensure all information is accurate and up-to-date. Double-check all figures and dates to prevent delays.

- Chronological Order: Organize documents chronologically, making it easy for the lender to follow the progression of your financial history.

- Clearly Labeled Documents: Clearly label each document with its type and date. This aids in quick identification and reduces confusion.

- Secure Storage: Store your documents securely to protect your sensitive financial information.

Negotiating the Best Mortgage Terms

Securing a mortgage with a low credit score often means navigating a more challenging landscape. However, effective negotiation can significantly impact your overall loan costs and terms. Understanding your leverage, communicating clearly, and thoroughly reviewing the contract are crucial steps in achieving the best possible mortgage terms. This section will outline strategies to help you negotiate a favorable interest rate and loan terms, effectively communicate with lenders, and understand your mortgage contract.

Strategies for Negotiating a Favorable Interest Rate and Loan Terms

Negotiating a mortgage involves more than simply accepting the initial offer. Several strategies can improve your chances of securing a better interest rate and more favorable terms. These strategies leverage your strengths and address potential lender concerns.

For example, a strong down payment demonstrates your financial commitment, potentially leading to a lower interest rate. Similarly, a stable employment history and consistent income stream strengthen your application and improve your negotiating position. Furthermore, shopping around for rates from multiple lenders allows you to use competing offers as leverage during negotiations. By showcasing your financial stability and demonstrating you are a desirable borrower despite your credit score, you increase your ability to negotiate better terms.

Effective Communication with Lenders

Clear and professional communication is essential throughout the mortgage process. This involves maintaining consistent contact, responding promptly to requests for information, and clearly articulating your needs and goals. Active listening is equally crucial to understanding the lender’s perspective and concerns.

For instance, clearly stating your financial goals and outlining your reasons for seeking specific loan terms can foster a more collaborative negotiation. Maintain a respectful and professional tone, even if you disagree on certain points. Documenting all communication, including emails and phone calls, provides a valuable record for reference. Consider preparing a concise summary of your financial situation and desired loan terms to share with the lender.

Understanding Mortgage Contracts

Thoroughly understanding your mortgage contract is paramount. This includes carefully reviewing all clauses, fees, and interest calculations. Don’t hesitate to seek clarification on any unclear terms or conditions. Understanding the implications of prepayment penalties, late payment fees, and other associated costs will allow you to make informed decisions.

For example, a common area of misunderstanding is the difference between fixed-rate and adjustable-rate mortgages (ARMs). Understanding the implications of an ARM’s fluctuating interest rate is critical in making a sound financial decision. Similarly, carefully examining the loan’s amortization schedule will help you understand the long-term cost of the mortgage. It is advisable to seek independent legal and financial advice before signing any mortgage contract.

Examples of Effective Negotiation Tactics

Several negotiation tactics can be employed to achieve favorable mortgage terms. Presenting a strong pre-approval letter from a competing lender can put pressure on the current lender to offer more competitive terms. Highlighting positive aspects of your financial profile, such as consistent income and low debt-to-income ratio, can also strengthen your position. Finally, demonstrating flexibility in your loan terms (e.g., considering a slightly shorter loan term) might increase your chances of securing a lower interest rate.

For instance, if you receive a pre-approval with a 5.5% interest rate from another lender, you can use that as leverage to negotiate a lower rate with your current lender. By showcasing your financial responsibility and willingness to compromise, you demonstrate your commitment and increase the likelihood of a successful negotiation.

Understanding Mortgage Insurance and Private Mortgage Insurance (PMI)

Securing a mortgage with a low credit score often necessitates mortgage insurance, a crucial element impacting your overall borrowing costs. Understanding the various types, costs, and implications of mortgage insurance is essential for making informed financial decisions. This section clarifies the purpose, costs, and workings of mortgage insurance, specifically focusing on Private Mortgage Insurance (PMI), commonly required for borrowers with less-than-perfect credit.

Mortgage insurance protects the lender against potential losses if you default on your mortgage payments. It essentially acts as a safety net for the lender, allowing them to mitigate the risk associated with lending to borrowers perceived as higher risk, such as those with lower credit scores. The implications for borrowers are increased monthly payments and, in some cases, extended loan terms. However, it also opens the door to homeownership for those who might otherwise be excluded.

Cost and Duration of PMI

The cost of PMI is typically expressed as a percentage of the loan amount and is added to your monthly mortgage payment. For borrowers with low credit scores, this percentage can be higher than for borrowers with excellent credit. The exact cost varies depending on several factors, including your credit score, the loan-to-value ratio (LTV), and the type of PMI. A higher LTV (meaning a larger loan amount relative to the home’s value) generally translates to a higher PMI premium. For example, a borrower with a 600 credit score and a 90% LTV might pay 1% of the loan amount annually in PMI, while a borrower with a 700 credit score and an 80% LTV might pay 0.5%. The duration of PMI is typically until you reach a certain level of equity in your home, usually 20% of the home’s value. This means you’ll pay PMI until your loan balance is reduced to 80% or less of the home’s appraised value. It’s important to note that refinancing your mortgage to a lower LTV can eliminate PMI.

Types of Mortgage Insurance

While PMI is the most common type of mortgage insurance for conventional loans, other forms exist. One key distinction is between Private Mortgage Insurance (PMI) and government-backed mortgage insurance, such as FHA insurance. FHA insurance is used for FHA loans, which are backed by the Federal Housing Administration and have more lenient credit score requirements. PMI is typically required for conventional loans when the down payment is less than 20% of the home’s purchase price. Both types protect the lender, but the costs and requirements differ significantly. FHA insurance premiums are typically higher and are paid monthly as part of the mortgage payment, but the initial down payment and credit score requirements are more flexible. Conventional loans with PMI usually have lower upfront costs but may require a higher credit score.

How PMI Works

PMI operates as a form of insurance that protects the lender in case of borrower default. If a borrower stops making payments, the lender can file a claim with the PMI insurer. The insurer then compensates the lender for a portion of the outstanding loan balance. This process allows the lender to recover some of their losses, minimizing their risk. The borrower, however, remains responsible for the remaining debt. The PMI premium is calculated based on a number of factors, including the loan amount, the borrower’s credit score, and the loan-to-value ratio. The insurer assesses the risk associated with each loan and sets the premium accordingly. The monthly premium is added to the borrower’s mortgage payment and paid directly to the insurer. Upon reaching the 20% equity threshold, the borrower can request the cancellation of PMI, thereby reducing their monthly mortgage payments.

Avoiding Mortgage Scams and Predatory Lending Practices

Securing a mortgage, especially with a low credit score, can be a stressful process. Unfortunately, this vulnerability makes some individuals targets for mortgage scams and predatory lending practices. Understanding these tactics and how to protect yourself is crucial to ensuring a fair and transparent mortgage process. This section will outline common scams, provide protective measures, and highlight warning signs to watch out for.

Common Mortgage Scams and Predatory Lending Tactics

Predatory lenders often target individuals with low credit scores or those facing financial hardship, preying on their desperation for housing. These practices frequently involve deceptive or unfair terms, resulting in significant financial harm. Common tactics include charging exorbitant fees, manipulating loan terms to increase the borrower’s interest rate, and employing high-pressure sales tactics. For example, a lender might promise a low initial interest rate that drastically increases after a short period, leaving the borrower with unsustainable monthly payments. Another example involves lenders adding hidden fees or charges not clearly disclosed in the initial loan agreement. These hidden costs can significantly inflate the overall cost of the mortgage.

Protecting Yourself from Fraudulent Lenders

Several steps can significantly reduce your risk of becoming a victim of mortgage fraud. Thoroughly researching lenders and comparing loan offers is paramount. Always independently verify the lender’s licensing and credentials through official regulatory bodies. Never rush into a decision; take your time to review all loan documents meticulously, and don’t hesitate to seek clarification on anything you don’t understand. Consider seeking a second opinion from a trusted financial advisor or mortgage broker who can help analyze the loan terms and identify potential red flags. Finally, be wary of lenders who pressure you into making quick decisions or who offer loans that seem too good to be true. A reputable lender will prioritize transparency and fairness throughout the entire process.

Red Flags to Watch Out for

Several warning signs can indicate a potentially fraudulent or predatory lender. These include high upfront fees or points that are disproportionate to the loan amount, unusually high interest rates compared to market averages, and lenders who pressure you to sign documents without fully explaining the terms. Other red flags include lenders who are unwilling to provide clear and concise answers to your questions, promises of guaranteed loan approval regardless of your credit score or financial situation, and requests for personal information over unsecured channels. A lender’s refusal to provide you with a written copy of the loan agreement or who tries to avoid discussing the terms and conditions should also be considered a serious warning sign. Finally, be suspicious of lenders who operate primarily online or through untraceable means.

Seeking Professional Financial Advice

Consulting a reputable financial advisor is highly recommended before committing to any mortgage. An independent advisor can provide objective guidance, help you understand your financial situation, and assess your mortgage options. They can help you compare different loan products, negotiate favorable terms, and avoid potentially harmful lending practices. A financial advisor’s expertise can save you from making costly mistakes and ensure you secure a mortgage that aligns with your long-term financial goals. They can also help you navigate the complexities of mortgage insurance and private mortgage insurance (PMI), ensuring you understand the implications and costs associated with these elements. Their unbiased perspective can be invaluable in navigating the often-complex world of mortgage lending.

Maintaining a Healthy Financial Situation After Securing a Mortgage

Securing a mortgage is a significant financial achievement, but it’s crucial to understand that the responsibility doesn’t end with the closing. Maintaining a healthy financial situation after obtaining a mortgage requires diligent planning, consistent effort, and a proactive approach to managing your finances. This section will outline strategies for effectively managing your mortgage payments, preserving a good credit score, and employing sound budgeting practices.

Effective Mortgage Payment Management

Successfully managing mortgage payments is paramount to avoiding late payments and potential foreclosure. Consistent and timely payments are vital for maintaining a positive credit history and avoiding financial penalties. Establishing an automated payment system, such as direct debit from your checking account, ensures timely payments and eliminates the risk of missed deadlines. Furthermore, creating a dedicated savings account specifically for mortgage payments can provide a buffer against unexpected financial challenges. Regularly reviewing your mortgage statement and contacting your lender immediately if you anticipate any difficulties is also recommended.

Maintaining a Good Credit Score After Mortgage Acquisition

Your credit score remains a crucial factor even after you secure a mortgage. A strong credit score can provide access to better financial products and lower interest rates in the future. Continuing to make all your payments on time, including credit cards, auto loans, and other debts, is fundamental. Monitoring your credit report regularly for errors and inaccuracies is also important, as these can negatively impact your score. Consider paying down high-interest debt to improve your credit utilization ratio, which significantly influences your credit score. Avoiding the opening of numerous new credit accounts within a short period is also crucial.

Budgeting and Financial Planning for Homeowners

Creating and adhering to a comprehensive budget is essential for successful homeownership. A well-structured budget allows for the allocation of funds towards mortgage payments, property taxes, homeowners insurance, and other home-related expenses. It also helps in managing other essential household expenses, such as groceries, utilities, and transportation. Regularly reviewing and adjusting your budget based on your income and expenses ensures financial stability. Consider using budgeting apps or spreadsheets to track your income and spending effectively. Planning for unexpected home repairs and maintenance is also vital, as these can be costly.

Sample Homeowner Budget Template

A well-structured budget should categorize income and expenses. Below is a sample template, which should be adapted to your specific financial circumstances.

| Income | Amount |

|---|---|

| Gross Monthly Income | $XXXX |

| Net Monthly Income (After Taxes) | $XXXX |

| Expenses | Amount |

| Mortgage Payment | $XXXX |

| Property Taxes | $XXX |

| Homeowners Insurance | $XXX |

| Utilities (Electricity, Water, Gas) | $XXX |

| Groceries | $XXX |

| Transportation | $XXX |

| Debt Payments (Credit Cards, Loans) | $XXX |

| Savings (Emergency Fund, Home Repairs) | $XXX |

| Other Expenses | $XXX |

| Total Expenses | $XXXX |

| Net Income After Expenses | $XXXX |

Remember to adjust this template to reflect your personal income and expenses. Regularly review and update your budget to ensure it accurately reflects your financial situation.

Last Recap

Securing a mortgage with a low credit score is achievable with the right knowledge and preparation. This guide has equipped you with the essential tools and strategies to navigate the process successfully. Remember, proactive credit management, careful lender selection, and diligent financial planning are key to securing a favorable mortgage and building a strong financial foundation for your future. By following the steps outlined, you can confidently pursue your dream of homeownership.